After a tumultuous few years of pandemic-related disruptions, 2024 has marked a sharp resurgence in deal activity, both in terms of volume and value, says Michael Amm, co-head of the M&A practice at Torys LLP.

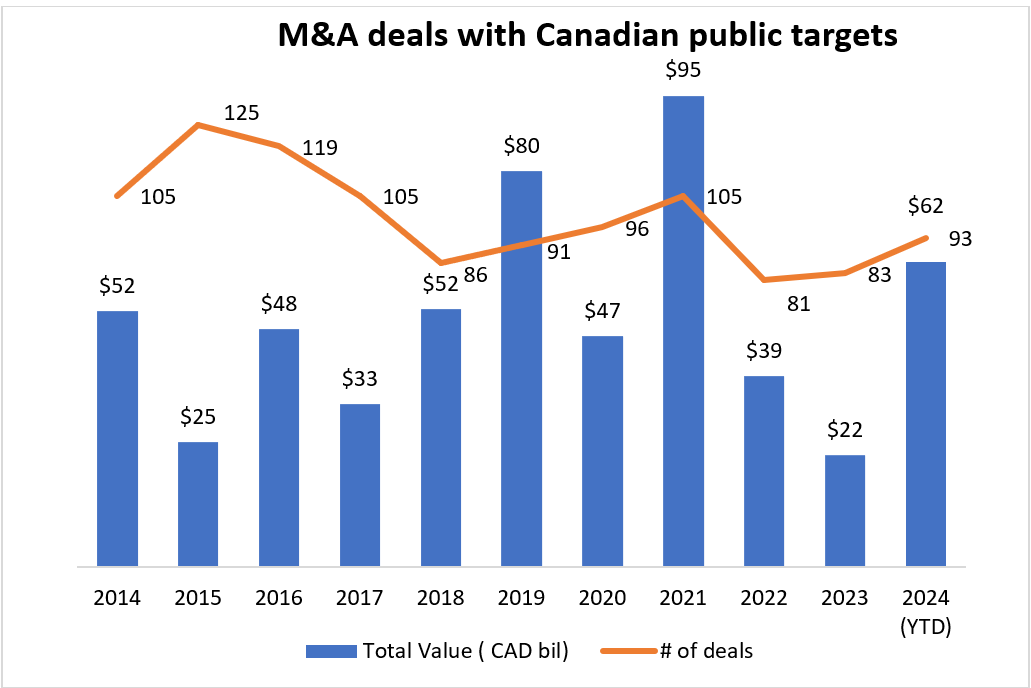

“In 2021, which was probably the biggest year by transaction value in the last decade,.. there were 105 deals with Canadian public targets, totalling $95 billion,” he says. But the following years saw a significant downturn, with deal values plummeting to $39 billion in 2022 and just $22 billion in 2023, alongside a drop in transaction numbers. “2024, by contrast, has started to grow very strongly,” he said, noting that 93 deals have already amassed $62 billion in value – indicators that deal-making is robustly rebounding.

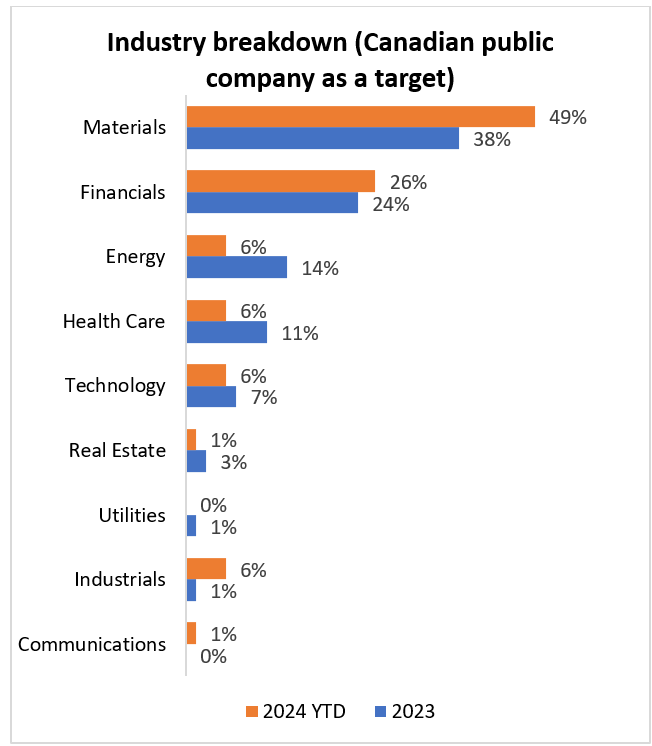

The resurgence isn’t merely a return to pre-pandemic levels; it represents growth beyond the norm. Deal sizes are notably larger, with transactions over $1 billion doubling compared to the last two years. Amm says materials, including mining and steel, accounted for almost half of M&A deals in 2024, followed by the financial sector. Major transactions like CI Financial’s $4.7 billion sale, Stelco’s sale to Cleveland-Cliffs for $3.5 billion, and several mining sector consolidations illustrate this trend.

Yet, this surge is not without its complexities. Foreign investment, while robust in terms of total deals, faces increased scrutiny, particularly from China. “There’s clearly an increased vigilance...particularly affecting buyers from China and Russia,” Amm says. Western nations, including Canada, are scrutinizing foreign direct investment with a focus on national security. Critical minerals, essential for industries like EV battery production, have become a flashpoint. “Canada and other Western countries have come out with some pretty strict investment screening on critical minerals deals,” Amm says, pointing to the failed Solaris deal as a recent example.

This pivot reflects a broader shift in global geopolitics and deglobalization trends. As nations seek to strengthen domestic supply chains, Canada has attracted significant investment, particularly in the auto and battery sectors. Federal incentives have drawn automakers like Volkswagen and Honda to establish large battery production facilities, cementing Canada’s role in the North American EV ecosystem.

However, regulatory environments have also grown more assertive. Whether through heightened competition reviews, as seen in cases like RBC’s acquisition of HSBC, or industry-specific interventions, deal-making now involves navigating an increasingly intricate legal landscape. “It’s certainly becoming harder, and that makes deals harder to do,” Amm says.

Another layer of complexity stems from shareholder activism, which Amm noted has intensified post-pandemic. Companies grappling with poor post-COVID performance have faced pressure from investors to adapt or sell. Additionally, many tech firms that went public during the pandemic have become acquisition targets following valuation slumps. These trends highlight a recalibration of market strategies, with boards showing greater discipline in pursuing sustainable transactions.

Macroeconomic conditions have played a pivotal role in shaping M&A dynamics. As inflation eases and interest rates stabilize, financing large-scale deals becomes more feasible. “A robust financing market...makes debt finance to fuel large M&A deals quite possible,” Amm says. While market stability fosters confidence, it also underscores the importance of strategic alignment. “There's a general sense of greater discipline amongst boards and management teams in terms of the transactions that they do, and that is a good thing for the space,” he says.

Looking south, Amm noted that a potential shift in US administration could influence deal-making, particularly if regulatory environments loosen under a second Trump presidency. However, cross-border transactions might face headwinds due to tariffs or trade policy shifts.

As for the future, Amm’s outlook is positive for dealmaking in Canada. “We have good conditions for M&A to continue its trajectory,” he says, citing falling interest rates and robust market fundamentals. “I'm optimistic, but there are things on the horizon that we need to watch out for pretty closely.”

Top 10 deals announced in 2024 by deal values

|

Deal Status |

Announce Date |

Completion/Termination Date |

Target Name |

Acquirer Name |

Announced Total Value ( CAD mil) |

Target Country/Region |

Acquirer Country/Region |

|---|---|---|---|---|---|---|---|

|

Completed |

4/1/2024 |

11/19/2024 |

Nuvei Corp |

Advent International Corp |

8553.51 |

Canada |

United States |

|

Pending |

11/25/2024 |

6/30/2025 |

CI Financial Corp |

Mubadala Investment Co PJSC |

8657.29 |

Canada |

United Arab Emirates |

|

Completed |

2/21/2024 |

6/4/2024 |

Enerplus Corp |

Chord Energy Corp |

5135.48 |

Canada |

United States |

|

Pending |

6/11/2024 |

12/31/2025 |

Canadian Western Bank |

National Bank of Canada |

5035.13 |

Canada |

Canada |

|

Completed |

1/19/2024 |

5/3/2024 |

Tricon Residential Inc |

Blackstone Inc |

4136.3 |

Canada |

United States |

|

Pending |

7/29/2024 |

3/31/2025 |

Filo Corp |

BHP Group Ltd,Lundin Mining Corp |

4110.74 |

Canada |

Australia |

|

Completed |

7/15/2024 |

11/5/2024 |

Stelco Holdings Inc |

Cleveland-Cliffs Inc |

3406.55 |

Canada |

United States |

|

Pending |

10/4/2024 |

3/31/2025 |

SilverCrest Metals Inc |

Coeur Mining Inc |

2040.72 |

Canada |

United States |

|

Completed |

3/19/2024 |

6/5/2024 |

Fusion Pharmaceuticals Inc |

AstraZeneca PLC |

2008.64 |

Canada |

United Kingdom |

|

Completed |

8/12/2024 |

10/30/2024 |

Osisko Mining Inc |

Gold Fields Ltd |

1827.73 |

Canada |

South Africa |

Source: Bloomberg, courtesy of Torys. Based on transactions involving acquisitions of Canadian public targets announced during Jan 1, 2014 - Nov 28, 2024. Excludes terminated and withdrawn transactions.