Credit: Thanaporn - stock.adobe.com

- What is the Statutory Accident Benefits Schedule?

- 1. Income Replacement Benefits (IRBs)

- 2. Non-Earner Benefits (NEBs)

- 3. Caregiver Benefits

- 4. Medical, Rehabilitation and Attendant Care Benefits

- 5. Death and Funeral Benefits

- 6. Optional Benefits

- 7. Payment of Other Expenses

- What are excluded from the Statutory Accident Benefits Schedule?

- Amounts of the Statutory Accident Benefits Schedule

Laws intervene to ensure that fairness in the insurance sector is kept, while protecting the rights and interests of both the insurers and their insured. In Ontario, its Statutory Accident Benefits Schedule not only helps in this goal, but also a lot more.

This article discusses the basics of this statute, as applied to both parties in an insurance contract. While getting the help of a personal injury lawyer is still best, this article is a good start for understanding this law.

What is the Statutory Accident Benefits Schedule?

The Statutory Accident Benefits Schedule (SABS) is one of the regulations under Ontario’s Insurance Act. Officially called the Statutory Accident Benefits Schedule — Effective September 1, 2010, it provides for the:

- specific benefits to insured victims of motor vehicle accidents

- amounts to each corresponding benefit

As for insurance companies, the SABS is one of their guides for coming up with a proper amount of compensation for their insured members.

Insurers and members should be abreast of the SABS, since some of its provisions are yet to come into force. For instance, Ontario Regulation 383/24, which amends the SABS will come into force by July 1, 2026.

Here’s a summary of the benefits under the SABS:

- Income Replacement Benefits (IRBs)

- Non-Earner Benefits (NEBs)

- Caregiver Benefits

- Medical, Rehabilitation, and Attendant Care Benefits

- Death and Funeral Benefits

- Optional Benefits

- Payment of Other Expenses

We’ll discuss each of these benefits below; you can directly skip to any benefits by using the table of contents above.

For a summary of what the SABS is all about, watch this video:

For more information about the SABS, talk to the best personal injury lawyers in Canada as ranked by Lexpert. This directory can be filtered per province and city.

Applicability of the Statutory Accident Benefits Schedule

A mandatory and no-fault insurance coverage, the benefits under the SABS must be written in every motor vehicle liability insurance policy. It covers all accidents that occur on or after September 1, 2010, while updated amounts are in place for those that occurred after June 1, 2016. Another set of changes will apply by July 1, 2026.

1. Income Replacement Benefits (IRBs)

The IRBs are given to those who sustain injuries because of vehicular accidents. These cover the following persons at the time of the accident, if the right conditions are met:

- employed or self-employed: the insured cannot perform essential employment tasks within 104 weeks (about two years) after the accident

- non-employed:

- if employed for at least 26 weeks (about six months) during the 52 weeks (about 12 months) before the accident; or

- if receiving benefits under the federal Employment Insurance Act; or

- if 16 years old or was excused from attending school under Ontario’s Education Act

If eligible, the insured will receive IRBs while unable to perform the essential employment tasks. The exempted periods would be the first week of the disability or after the first 104 weeks (about two years) of disability, unless it becomes long-term.

However, an insured is not eligible for IRBs if they chose to receive the NEBs or caregiver benefits instead.

2. Non-Earner Benefits (NEBs)

NEBs are given to an insured who sustains an impairment if they cannot carry on a normal life within 104 weeks (about two years) after the accident, and they either:

- do not qualify for the IRB

- was educationally enrolled full-time at the time of the accident

- has completed their education less than one year before the accident, and was neither employed nor self-employed person after completing their education and before the accident

3. Caregiver Benefits

Caregiver benefits are given to the insured if:

- they sustained a catastrophic impairment

- they're the primary caregiver for and is living with a person in need of care

- they're not receiving any payment for these caregiving activities

4. Medical, Rehabilitation and Attendant Care Benefits

Under the SABS, the insured must pay the medical, rehabilitation, and attendant care benefits to the insured. The most common requisite among these three is that these should be reasonable and necessary expenses incurred by the insured.

5. Death and Funeral Benefits

Death benefits are given to the insured’s spouse or dependents if the insured died:

- within 180 days (about six months) after the accident; or

- within 156 weeks (about three years) after the accident, if during that period the insured was continuously disabled because of the accident

6. Optional Benefits

In addition to the standard automobile coverage under the SABS, there are other optional coverage for the parties involved. These may increase or improve the existing SABS benefits but are subject to certain conditions.

7. Payment of Other Expenses

Aside from the ones mentioned above, there are other expenses that the insurer must pay, such as the insured’s:

- lost educational benefits

- expenses of visitors

- housekeeping and home maintenance

- damage to clothing, etc.

- cost of examinations

What are excluded from the Statutory Accident Benefits Schedule?

The SABS also sets out some instances where insurers do not have to pay certain benefits. It provides that IRBs, NEBs, and some of the other expenses may not be paid in the following cases:

-

if the driver:

- knew, or ought reasonably to have known, that the vehicle is not insured

- was driving without a valid driver’s license

- is excluded under the automobile insurance contract

- was driving the vehicle without its owner’s consent

-

in respect to any person:

- if there’s material misrepresentation that induced the insurer to enter the automobile insurance contract

- if they’re engaged in a criminal act at the time of the accident, and was convicted for such offense

- if they did not follow the demand of a police enforcer for a roadside coordination test, breath screening test, or drug screening test

-

in respect of an occupant:

- if they knew, or ought to have reasonably known, that the driver was driving the vehicle without its owner’s consent

A criminal offence under the SABS is not just limited to driving under the influence of drugs and/or alcohol. It also includes other offences under the Criminal Code, whether related to motor vehicles or not.

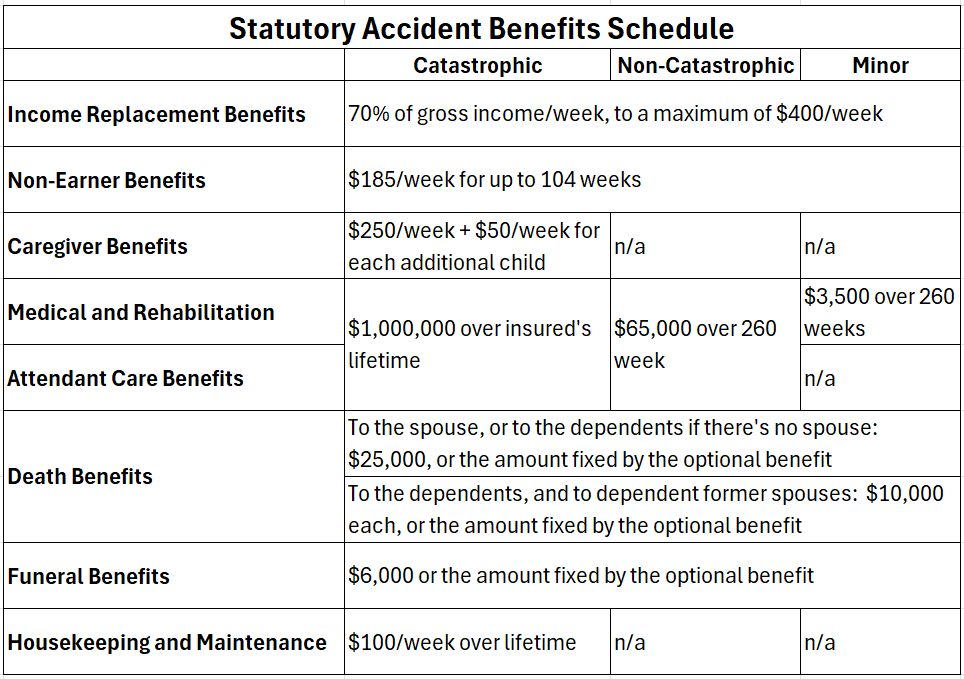

Amounts of the Statutory Accident Benefits Schedule

As for accidents that occur and for insurance policies that are renewed after June 1, 2016, below is the amount under each benefit in the SABS:

For the specifics of this table, it's better to have an independent legal counsel, aside from inquiring with your insurance company.

Learn more about the Statutory Accident Benefits Schedule, as applied to your case, by reaching out to a Lexpert-ranked best law firms in Canada for personal injury cases.