Even for tech companies that may not be directly impacted by US tariffs, uncertainty still clouds deal-making. However, M&A lawyers in the tech space say the momentum of a growing technology sector, fuelled by advances in artificial intelligence, continues to drive optimism in the longer term.

Zain Rizvi, partner at Davies Ward Phillips & Vineberg LLP, whose M&A practice spans both software and hardware technology deals, says that tariff-related uncertainty is prompting more conservative valuations for some companies as buyers weigh the potential impact of tariffs. “It’s challenging to agree on what a company is worth if profits could take a hit due to tariffs.”

However, Rizvi notes that most of the caution is concentrated on the manufacturing side of the tech sector, where companies are more exposed to cross-border trade. “For technology services and software companies, there is still strong momentum for M&A, in part because they are seen as less directly impacted by tariffs.”

On the other hand, Rizvi says that deals involving companies that may be directly or indirectly affected by tariffs are more often “being put on pause or taking longer to complete” as more time is needed to assess the potential impact on customers, import costs, and profit margins.

“One of the key questions is whether customers, especially those facing cost pressures from tariffs, still have the budget to spend on the technology. That affects not just hardware and tech-enabled products, but software companies too.”

He adds that some companies are taking a “wait and see” approach to the tariff threat, particularly on deals with high US exposure. “Right now it is all very fresh,” Rizvi says. “Some buyers may decide to wait a quarter or two to see how this all plays out.”

Still, Rizvi notes that deal activity remains strong for companies involved in areas like artificial intelligence, with multiple startups continuing to attract acquisition interest.

“Many people in the tech sector are taking a long-term view and see these tariffs as temporary. They don’t want to shelve or derail growth plans because of a trade squabble that may soon be resolved. Some buyers may see lower valuations as an opportunity to acquire good companies at a discount.”

He adds that AI-focused companies may be particularly appealing in this environment, especially if their technologies help drive efficiencies that offset the negative impact of tariffs.

Heidi Gordon, who co-leads the national tech M&A practice at McCarthy Tétrault LLP in Toronto, notes that the level of volatility has changed since the end of last year, when Donald Trump was elected as president of the United States and went on to impose massive tariffs on most countries as part of his desire to change the current order of world trade. “There’s a lot of volatility, not just domestically but globally, and volatility on this scale affects all sectors, including tech,” she says.

Gordon says this volatility contributes to increased uncertainty around the trajectory of interest rates, the value of currencies, and the reception to foreign investment. These can all be key drivers of deal-making and valuations, particularly for a country like Canada, where there has historically been a considerable amount of cross-border deal activity.

Even the recent election of another minority government in Canada, this time under former central banker Mark Carney as prime minister, still leaves the question of how Canada will respond to Trump’s aggressive moves on everything from tariffs to comments about wanting Canada to become “the 51st state.”

Also, while software companies have so far been relatively immune from tariffs imposed by the United States, Gordon notes that “some enterprise software businesses also have a hardware component, which may be impacted by tariffs.”

On the other hand, the opportunities presented by AI should not be ignored. “The adoption of AI has accelerated across all sectors, enhancing the value, importance, and relevance of the tech sector.”

Gordon acknowledges that continued uncertainty lies ahead and notes that deal activity in the tech sector has been up and down throughout the first part of this year. And while tools such as earnouts, deferred purchase price arrangements, and seller rollovers can help solve a valuation gap between motivated buyers and sellers, “we’ll likely see deal-makers treading carefully over the course of the next several months.”

Ottawa-based Andrea Johnson, global co-head of Dentons’ private equity group, says her personal experience over the past months is that her M&A business is “quite brisk.” She believes that “M&A decision-makers, for the most part, feel that the trade war may create a difficult sort of environment, but that it is temporary – they are optimistic it will blow over.”

She adds that deal-makers “don’t want to lose time by not being engaged, so they are going ahead and doing deals, but it is based on a guess that the environment will normalize or at least stabilize. They don’t want to pass up opportunities.”

Johnson notes that Canada has a lot of strength in the software sector, including a strong software as a service sector (SaaS), an area that is less likely to be impacted by the current US tariffs, at least directly. There is also an emerging cohort of AI companies that could be part of deal-making in the sector.

However, she also acknowledges that recession fears could impact M&A activity. Deal-makers may want to slow down until the landscape becomes more apparent, and what deals come to the table will probably undergo substantial due diligence.

Johnson notes that increasing reliance on risk-aversion tools such as earnouts will likely continue, adding, “We’re seeing higher earnout clauses as a portion of a deal value” as they become part of the negotiating process.

Regarding the valuation gap between buyers and sellers, “our advice is always to have the difficult conversations upfront about how the business is going to be supported under its new ownership – what are the success factors needed that can be committed to by both parties.”

The due diligence process has also changed in recent years and is perhaps more rigorous than the compressed process a few years back, “when competition was fierce and the deals were coming fast and furious.

“There’s still competition for high-quality targets, but there’s been a return to what I would call a normal intensity, compared to the more ‘wild’ days of two or three years ago.”

Joanna Myszka, partner with Blake, Cassels & Graydon LLP based in Montreal, agrees that parties involved in M&A in the tech sector are “looking at ways of mitigating risks and bridging the valuation gaps through different mechanisms.”

These can include purchase price reductions, earnouts, deferred payments, and “rollover equity.” The latter is a deal structure in which sale proceeds from an acquisition are reinvested by the seller into the newly formed company rather than being paid out. The seller retains an ownership stake in the new entity and participates in its future growth.

Says Myszka: “Other tools that can be used include increased diligence, an enhanced review of sector-specific issues, and the use of tailored representation and warranties insurance.”

However, while Myszka sees added caution in deal-making and parties might be slower to kick off discussions and get through the diligence stage, “once the parties have aligned on the business terms and want to go forward, the pace marches more along the lines of what we’re used to seeing.”

Even with the current uncertainty, Myszka says she’s seen “quite an uptick in new deals and projects that have come across my desk, which is encouraging for the 2025 deal pipeline.”

Much of Myszka’s practice deals with private equity, and she notes that it has a lot of capital to deploy and is very interested in companies that are less vulnerable to tariffs. These companies include services businesses that rely on intellectual capital, such as software, IT services, and video game content development.

Strategic buyers, on the other hand, “are more likely to focus on predetermined strategic plans and what they feel their company needs to move forward.”

Ultimately, Myszka says that while it’s hard to predict the future, she shares the optimism of most of her clients and those in the tech sector who have seen significant disruptions to the economy over the years, from the financial crisis of 2008 to the more recent COVID-19 pandemic.

“I think people in the corporate world will continue running their businesses and engaging in the activities needed to grow their business, even if the circumstances change and adjustments are required, including M&A and deal-making.”

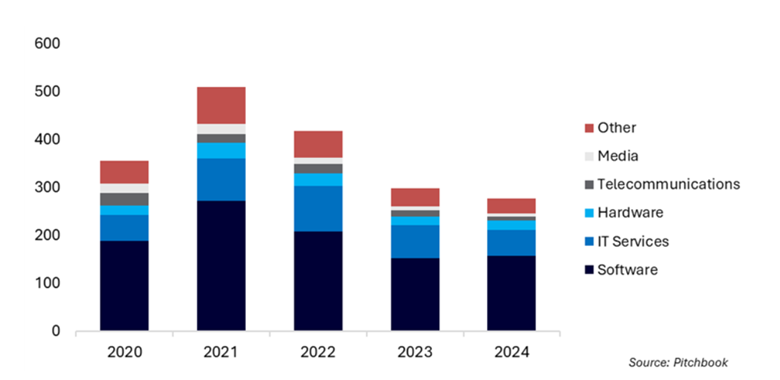

Canadian tech M&A activity, 2020–2024 – Number of deals